May 27, 2026 • 8 min read

Gartner Magic Quadrant for CPaaS 2026: Top Takeaways

Director of Content & Market Research

May 27, 2026

95% of global enterprises will leverage communications platform as a service (CPaaS) to operationalize customer experience and engagement by 2029. That’s up from 60% in 2025.

Yet, while Gartner’s big prediction that opens its latest CPaaS Magic Quadrant paints a rosy picture, the truth is that the market is in a state of significant flux.

CPaaS adoption has long been driven by piecemeal implementations, with many providers relying heavily on legacy revenue streams such as SMS APIs. As those face rapid commoditization, vendors are being forced to isolate where they fit in the future enterprise stack and climb the value chain.

For many vendors, that means scaling newer messaging formats like RCS and delivering Network APIs, while also expanding into new arenas, such as AI orchestration, voice automation, and data platforms. It's a significant shift, not just in product terms, but in who vendors are marketing to, how they structure support, and how they price.

Below is an overview of the vendors Gartner identifies as leading this shift, followed by a closer examination of where the market is headed.

Who Are Gartner’s CPaaS Market Leaders in 2026?

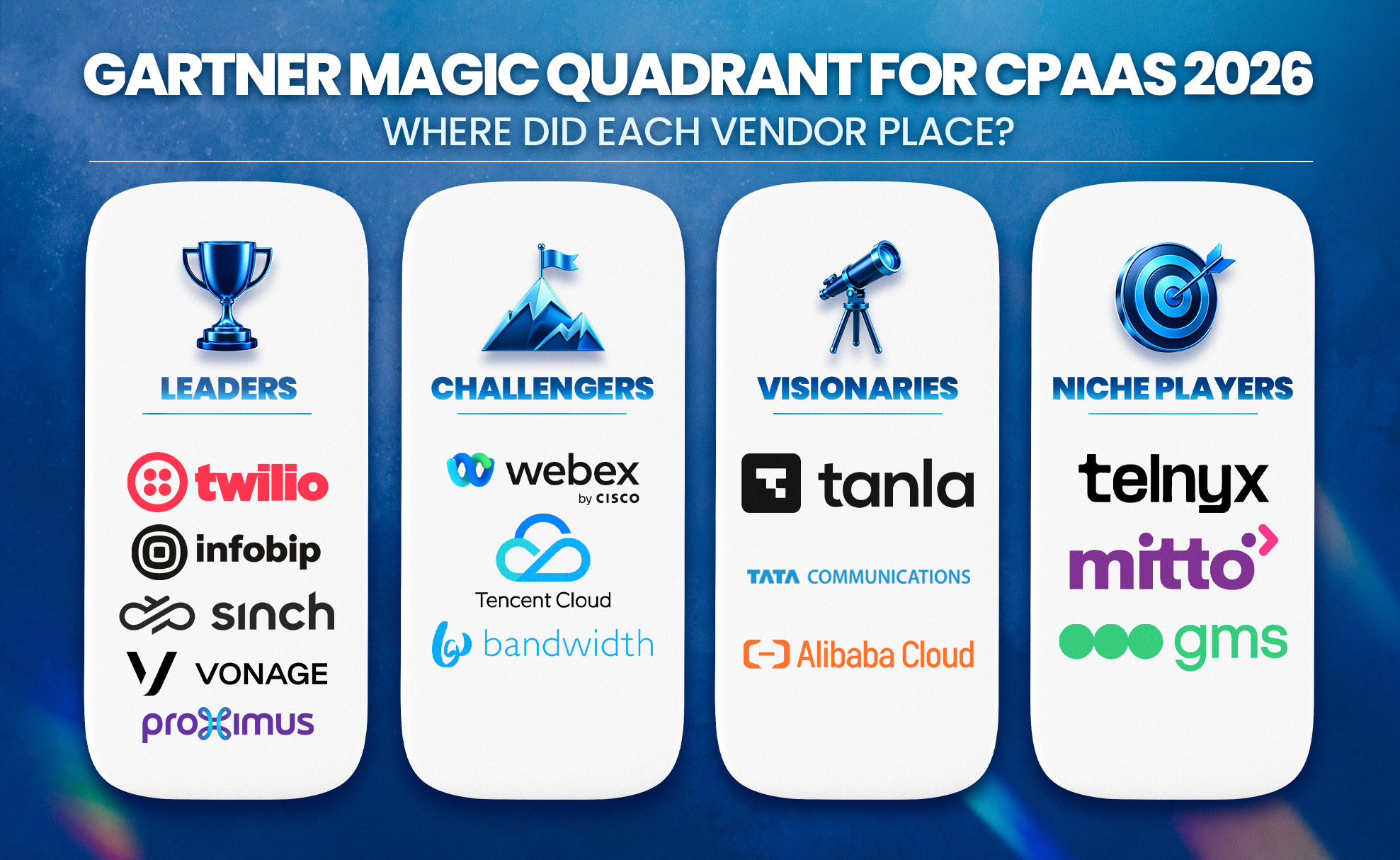

The Gartner Magic Quadrant identifies five market leaders: Twilio, Infobip, Sinch, Vonage, and Proximus Global.

One major reason for Twilio’s leadership is its integration with Segment, its customer data platform. Together, they combine customer data, messaging, and voice capabilities in powerful ways. A strong example is Twilio Predictions, which helps businesses anticipate customer behavior and take proactive steps to influence journey outcomes.

Similarly, Infobip offers a native CDP. However, Gartner highlights its early adoption of MCP servers and involvement in MCP standards, which it says has given the company an early advantage in AI agent development and orchestration, an area many see as the next frontier for CPaaS.

Sinch stands out for its ecosystem, with Gartner highlighting its 1,000+ active partners and 500+ integrations across enterprise systems and carrier networks. The analyst also commends its advanced security capabilities.

The other two leaders are new to the top-right quadrant, having placed as visionaries last year.

Like Infobip, Vonage earns praise for its “AI-ready” APIs and MCP servers. Surprisingly, however, Gartner makes no mention of its advanced Network APIs, which enable emerging CPaaS use cases such as identity verification, SIM-swap detection, and real-time translation.

Lastly, Proximus Global gains credit for its expansive communications channels, “high-performance” global network, and presence across all continents (except Antarctica!). Much of this is the result of its acquisitions of BICS, Telesign, and Route Mobile, which it continues to pull together.

The remaining nine vendors evaluated by Gartner are grouped in the image below.

Despite significant shifts in the CPaaS space, the groupings are not vastly different from 2025. Although alongside the two new leaders, Cisco shifts from a visionary to a challenger.

There are also new additions in Alibaba, Telnyx, and GMS, with the former racing into the visionary category.

Still, many notable market players miss out. These include Bird, CM.com, Comviva, Microsoft, and Plivo, all of which are global CPaaS providers.

7 Top Takeaways from the Gartner Magic Quadrant for CPaaS 2026

Seven key takeaways emerge from Gartner’s evolving CPaaS definition, revised evaluation framework, and updated vendor analysis. Below is an original analysis of each.

1. The Magic Quadrant Is Notably Less Developer-Focused Than Previous Years

In 2025, Gartner explicitly called out "developers, the IT team, and other nontechnical business roles" as the intended users of CPaaS solutions. This year, it simply says “businesses”.

That pivot is likely intentional, removing CPaaS further from its origin story as a developer-focused technology category.

Players like Twilio pioneered the category by establishing vibrant builder communities, robust Software Development Kits (SDKs), and developer-focused documentation.

Over time, this “hoodies and community” culture became a core competitive advantage, with developers choosing a platform and then building on it.

Yet, AI is transforming the category, with AI agents, not human developers, starting to consume APIs and SDKs.

These AI agents don’t care about documentation quality, SDK elegance, or developer marketing. They may even interpret or even reverse-engineer APIs on their own.

Over time, they promise to choose providers dynamically to optimize cost and quality across geographies, posing a problem for CPaaS providers stuck in the past.

Rob Kurver, Founder of the CPaaS Acceleration Alliance, referenced this trend in a similar market overview, underscoring how the industry is on the cusp of a major transformation.

“The whole concept of being appealing to developers, that whole moat, is gone in a new world where AI rules."

2. AI Orchestration Becomes a Key Battleground for CPaaS Providers

In a bid to become more deeply embedded with customers, vendors appear to be competing primarily across two key battlegrounds: network depth and AI orchestration.

The latter sees more CPaaS providers lay down a communications infrastructure over customer-facing departments to connect systems, share data, and coordinate AI agents and workflows.

As they do so, Gartner suggests that differentiation will ultimately depend on "trusted engagement, seamless integration, and measurable business outcomes.”

By making this assertion, Gartner implies that pure technical capability will commoditize, and that outcome delivery will become the new competitive moat.

Of course, network depth will also remain a significant differentiator between vendors.

Nevertheless, Gartner seems downbeat on the penetration of Network APIs, noting that: "This has not transformed into large-scale adoption yet." That said, it’s still a key industry trend to keep in focus.

3. Gartner Downgrades Providers Not Supporting MCP Servers

Businesses may blend CPaaS capabilities across multiple vendors as MCP wrappers and AI orchestration become more commonplace.

Gartner recognizes this as a significant shift, specifically applauding Infobip, Vonage, and Sinch for their MCP server support and signaling that AI agent discoverability and interoperability are becoming meaningful differentiators.

Conversely, it also flags vendors without MCP support as behind, explicitly cautioning Proximus Global on this, despite pegging the provider as a market leader.

Another notable architectural trend is Gartner’s recognition of vendors shifting toward edge processing over centralized cloud deployments to improve real-time AI performance, an area it did not highlight in its 2025 report.

4. Voice AI Emerges as a Key Growth Opportunity

In 2026, Gartner added several new optional voice capabilities to its evaluation framework. These include AI workflow automation with smart routing, dynamic IVR, self-service flows, Text-To-Speech (TTS), and Speech-To-Text (STT).

By doing so, it underscores how quickly CPaaS providers are building out their voice AI capabilities, transcribing contacts, analyzing interactions, and unlocking insight.

Some are also extending into voice automation, sensing an opportunity to compete in the self-service space with conversational AI vendors.

CPaaS providers have an advantage in their ability to blend channels, orchestrate workflows across systems, and deliver low-latency, high-accuracy voice conversations.

That said, there is significant competition from conversational AI providers, from stalwarts such as Google, Kore.ai, and NiCE Cognigy to disruptors like Decagon, Sierra, and Crescendo.

5. Pricing Transparency and Support Become Common Friction Points

In 2025, Gartner’s pricing analysis largely focused on SMS rate increases and the shift toward “carrier-plus” models bundling network and CPaaS solutions.

By 2026, the conversation has matured, with vendors investing in AI orchestration and moving toward outcome-based pricing. This is a meaningful shift, suggesting that the overall CX market transition toward value-based commercial models rather than pure usage-based ones is now expanding into the CPaaS space.

However, Telnyx is the only vendor called out positively for its pricing approach. While it still only offers usage-based pricing, the vendor receives praise for its transparent model.

The model comprises separate pay-as-you-go and volume-based pricing plans. Both include automatic discounts, 24/7 support, and Mission Control Portal access, while volume-based customers also receive custom rates, dedicated support, and prioritized assistance.

Elsewhere in the report, other vendors, including Twilio and Vonage, are dinged for being expensive, despite both achieving “leader” status.

Meanwhile, inconsistent or weaker support is flagged as a concern for Alibaba, Cisco, Bandwidth, GMS, Infobip, Sinch, and others. This is striking, though perhaps not entirely surprising.

After all, the shift from a “here’s some documentation, figure it out with the community” model to something far more complex, i.e., customer experience and AI orchestration, is not an easy transition to make.

6. Gartner Places Much More Emphasis on CDPs and IoT

In previous editions of the Magic Quadrant, CDP and IoT (Internet of Things) capabilities were only a footnote.

Now, Gartner outlines audience segmentation, AI-driven personalization, next-best-action recommendations, and customer journey analytics amongst its evaluated features.

As such, it’s perhaps no surprise that Twilio and Infobip have surged further ahead of the competition in the “leader” bracket, both with native CDPs.

Meanwhile, from an IoT perspective, Gartner considered device-to-cloud APIs, SMS/WhatsApp notifications for IoT sensor events, voice-control APIs for smart devices, and video streaming APIs for cameras. It didn’t reference any such capabilities specifically in 2025.

Again, this expands the scope of CPaaS into orchestrating data, tools, and AI agents, paving the way for more intelligent communications.

7. Vertical-Specific Knowledge Becomes More of a Differentiator

Several providers position vertical-specific expertise as a key differentiator. Examples include Tata Communications in financial services and Tencent Cloud in gaming, where their respective strengths in support services and low-latency audio/video align closely with industry needs.

This kind of verticalization is becoming increasingly common as the market matures and horizontal offerings become commoditized. Regulated industries especially favor vendors that have already addressed compliance requirements.

Traditional differentiators such as network ownership, carrier relationships, and omnichannel capabilities remain important, but partner ecosystems and marketplace integrations are also emerging as major competitive advantages.

Gartner underscores this by lauding Sinch, Twilio, Tata, and Vonage for their ecosystem depth, repeatedly citing Salesforce, SAP, Microsoft, Adobe, and CCaaS platforms as key systems to offer robust integrations with.