April 22, 2026 • 9 min read

Forrester Wave for Conversational AI Platforms, Customer Service 2026: Top Takeaways

Director of Content & Market Research

April 22, 2026

Conversational AI platforms are shifting from answering questions to completing tasks.

That’s a fundamental transformation, and many of the 650+ global conversational AI providers serving customer service and sales teams are embracing agentic frameworks to enable this change.

Yet, as they race toward these new frameworks, enterprises still need more mature integrations, data strategies, and analytics.

Meanwhile, conversational AI stalwarts face new competition. Well-funded entrants aim to eat off their plates with platforms built in the agentic AI era.

As such, the entire market is in a state of flux, and Forrester aims to support buyers with an analysis of “the most significant” platform providers in the space.

The research firm breaks down its analysis across two core criteria: strength of strategy and strength of offering, with 22 sub-criteria.

In doing so, it surfaces several fascinating trends across the space, while also spotlighting three market leaders.

Who Are Forrester’s Conversational AI Market Leaders in 2026?

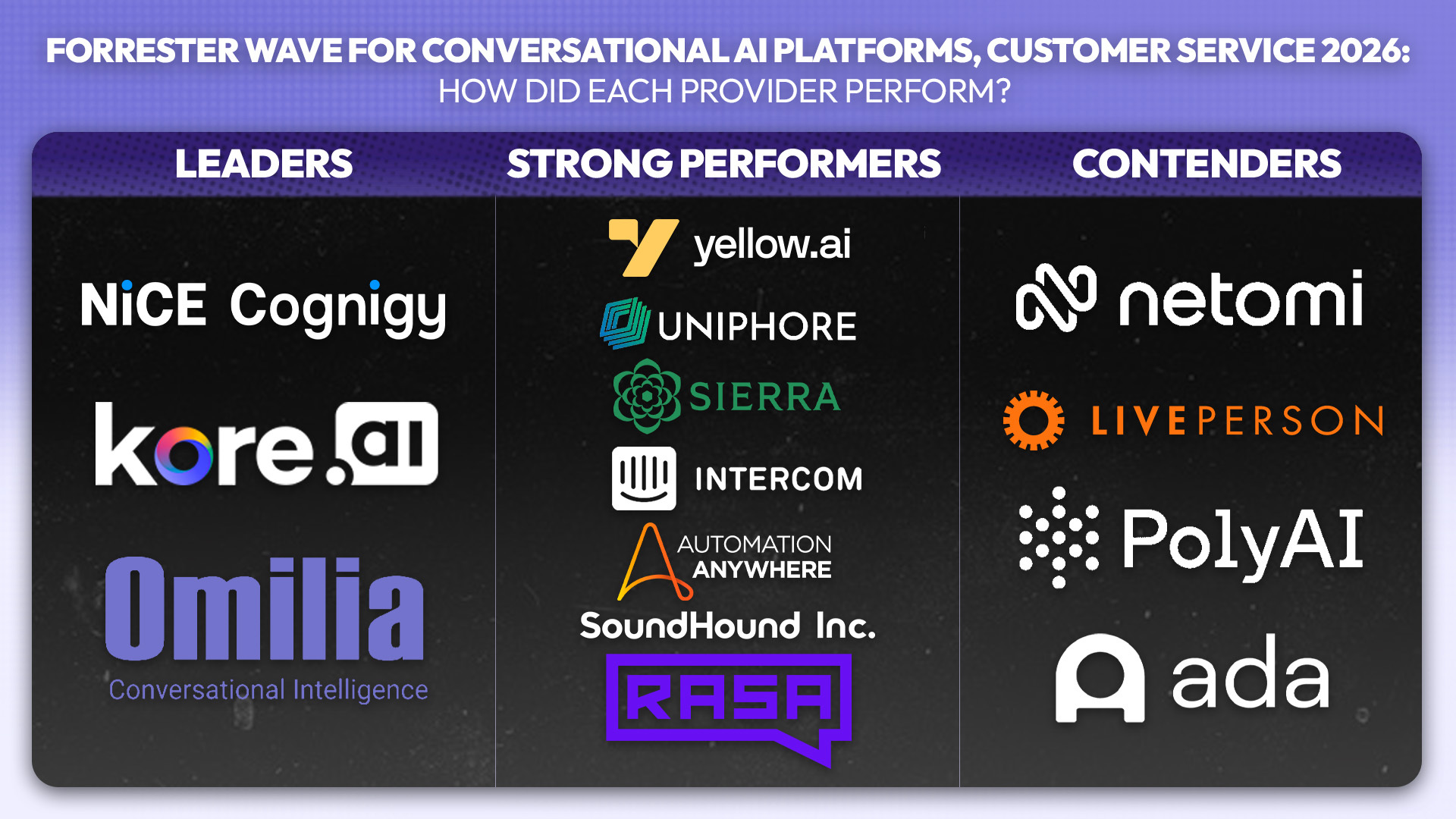

The Forrester Wave isolates three market leaders: NiCE Cognigy, Kore.ai, and Omilia.

NiCE Cognigy leads on its strength of strategy. NiCE is a CCaaS and Workforce Engagement Management (WEM) leader, and Forrester recognizes the potential for Cognigy to apply its AI across NiCE's portfolio. For instance, a single WEM platform for human and AI agents is a compelling prospect, which is on NiCE‘s roadmap.

Meanwhile, Kore.ai leads on its strength of offering, with Forrester explicitly commending its AI model management (blending first-party LLMs and SLMs), governance features, and back-end system integrations.

Omilia also sweeps into the leader group thanks to its “significant OEM relationships”, customer support services, and experience in delivering edge use cases.

The other 11 evaluated vendors are outlined in the image below, as Forrester grouped them.

Forrester last released a Wave study for conversational AI in customer service two years ago. Aside from Cognigy and Kore.ai maintaining their leader positions, the latest report is drastically different.

Indeed, Onereach.ai, a previous leader, is no longer included. Meanwhile, Sprinklr, Avaamo, Verint, and eGain all drop off.

Conversely, Sierra, Uniphore, Intercom, and Rasa enter as “strong performers”, while Poly.ai and LivePerson are also included for the first time.

Again, this highlights the state of flux within the market, with big names such as Google, Decagon, and Boost.ai not included.

Yet, that’s just one takeaway from the report. Several others emerge after a closer inspection of the individual vendor analysis Forrester presents.

7 Top Takeaways from the Forrester Wave for Conversational AI, Customer Service 2026

From the vendor analysis in the 2026 Forrester Wave study, seven overarching trends emerge in the conversational AI market. Here is an original analysis of each.

1. Conversational AI Pricing Strategies Lack Maturity

One of the criteria Forrester uses to evaluate conversational AI providers’ strategy is “pricing flexibility and transparency.” Notably, only one vendor scored above three out of five in this category: Rasa.

Rasa stands out with a freemium approach, which allows organizations to build and validate AI agents at no cost. It also offers a Free Developer Edition for teams handling fewer than 1,000 contacts per month, lowering the barrier to experimentation and early-stage deployments.

While there are perhaps lessons to learn from Rasa, Forrester’s report ultimately underlines that pricing models for conversational AI still lack maturity. Instead, vendors continue to experiment across several common approaches:

- Per-agent pricing: A subscription model that mirrors traditional contact center seat-based pricing.

- Per-action pricing: A consumption-based model where costs scale with each task the agent performs.

- Per-workflow pricing: Similar to per-action, but tied to the completion of defined multi-step processes.

- Per-resolution pricing: A performance-based model where charges apply when an interaction is successfully resolved.

- Per-minute pricing (voice agents): A time-based model, typically with tiered rates based on usage.

Looking ahead, the vendors most likely to win on pricing will be those that combine flexible pricing structures with clear, granular ROI analytics.

2. Personalization Is Another Area for Improvement

Forrester commends Netomi for its “superior capabilities for managing customer data to enable personalized customer interactions.”

Yet, this is a single standout mention in Forrester’s vendor analysis for personalization, reinforcing how it’s rarely positioned as a defining strength.

That’s surprising, as there is a significant opportunity here. Instead of plugging into a CRM for context, utilizing a coordinated customer data platform (CDP) would enable better-informed, truly individualized experiences.

For instance, an agent with data pulled into a CDP via an ERP solution may note that a customer’s recent bill was unusually high and anticipate that query.

There’s also an opportunity to pull in real-time data to personalize customer interactions, especially on the voice channel.

For instance, if the customer sounds nervous, can the voice agent soften its tone? If the customer is speaking quickly, as if in a rush, could the agent match the speed?

Providers rarely offer such capabilities, and CX Foundation underscored this opportunity in its recent conversational AI market overview.

3. Sierra Breaks Through as an Industry Disruptor, Others Don't

Founded in 2023, Sierra, led by former Salesforce co-CEO Bret Taylor, is already valued at $10 billion, winning over companies aspiring to jump straight to agent-first architectures rather than evolving legacy stacks.

While Sierra earned a “Strong Performer” commendation, the absence of other providers, born in the AI agent era and already winning significant enterprise business, is a notable gap in the 2026 Forrester Wave report.

Take Decagon as an example. Also founded in 2023, it has already reached a $4.5 billion valuation and is winning major enterprise clients such as Deutsche Telekom with its concept of Agent Operating Procedures (AOPs).

AOPs allow CX leaders to define their desired experiences in natural language, which are then translated into code that IT teams can use to set rules, enforce guardrails, and integrate with backend systems. The result is a unified operating model that helps cut through the internal friction over who owns the conversational AI strategy.

Alongside Decagon, Crescendo.ai is another big disruptor. Launched in 2024, it already earns over $100 million in annual recurring revenue (ARR).

Crescendo’s promise is no workflows, decision trees, pseudo-code, or step-by-step orchestration. It doesn’t even use structured abstractions, like Decagon’s AOPs. Instead, it’s entirely based on behavior prompts, a knowledge base, tool access, and policies (i.e., guardrails), claiming to enable more flexible reasoning and better handling of edge cases.

As these brands are new to the market and so differentiative, Forrester is perhaps exercising caution by not including them. Nevertheless, expect to see them in future editions, as rare visionaries in an overcrowded market.

4. Integrations with Legacy Systems Are a Blocker for Many

Enterprises run on complex backend systems, and AI platforms must integrate them seamlessly. Yet, this remains a persistent blocker, particularly for more disruptive vendors.

For example, while Sierra earns top marks for its agentic framework, vision, and roadmap, it scores just one out of five for legacy system integrations.

Three other vendors receive similarly low scores for legacy integrations, and this limitation can result in scalability constraints, difficulty supporting complex workflows, and a greater reliance on external tools and workarounds.

By contrast, Intercom, Kore.ai, and Yellow.ai score highly for their legacy integration capabilities. Yellow.ai’s approach is particularly notable, using an on-premises “translator” application to bridge its platform with legacy systems.

However, the integration conversation is increasingly shifting beyond basic connectivity toward orchestration.

Rather than simply linking systems and pushing or pulling data via APIs, the focus is moving toward coordinating agents across multiple systems, managing end-to-end resolutions across tools, and enforcing safety and guardrails across chains of agents.

How vendors adapt to and operationalize this shift will be critical to their long-term competitiveness.

5. Conversational AI Providers Play Catch-Up on Reporting and Analytics

Many conversational AI providers deliver agentic frameworks faster than they can measure their end-to-end impact, leading companies to rely on external business intelligence (BI) solutions.

Even customers of NiCE Cognigy, which leads the Forrester Wave overall, reported that they export data to tools like Tableau to report on changing outcomes outside the contact center.

That said, NiCE does offer a compelling vision for managing and monitoring human and AI agents as part of a unified WEM solution. Nevertheless, for now, many customers are working to complete the analytics layer - and this is an industry-wide trend.

For instance, feedback on Yellow.ai and LivePerson highlights an over-dependence on third-party reporting for enterprise customers.

Moreover, Forrester doesn’t explicitly note analytics as a core strength of any vendor in the report, which perhaps spotlights end-to-end outcome measurement and CX insight as an opportunity for differentiation.

6. Providers Learn That Speed-to-Value Is a Key Differentiator

Many of the strengths Forrester outlines across vendors relate back to speed-to-value, as vendors optimize for faster deployment, lower upfront effort, and earlier ROI.

The analysis points to three primary ways vendors are achieving this.

First, through prebuilt components that reduce the need for customization. Intercom stands out here, with a library of prebuilt elements that help accelerate deployment timelines.

Second, through AI-assisted development. The report highlights compelling examples from Yellow.ai and Uniphore. Yellow.ai’s Nexus AI assistant helps identify, prioritize, and test applications, while Uniphore offers tools that can surface use cases, model them, test performance, and even provide scoring and recommendations for improvement.

Finally, vendors are rethinking deployment models altogether. For example, Sierra forward-deploys engineers to reduce implementation friction and accelerate adoption.

Faster utterance generation and pre-trained intents are other ways conversational AI providers can accelerate deployments. Boost.ai and DRUID AI are examples of vendors outside the report that excel here.

7. Consolidation and Platformization Are Accelerating

Many of the vendors included in this report shifted into the conversational AI space through acquisitions. For instance, NiCE acquired Cognigy, Automation Anywhere picked up Aisera, and SoundHound snagged Amelia, Interactions, and (most recently) LivePerson.

This isn’t a random trend; these vendors are assembling full-stack capabilities to satisfy enterprise demand for fewer vendors, tighter integrations, and unified governance.

Also, by pooling their capabilities, vendors can bring unique capabilities to market. For instance, NiCE can utilize its workforce management (WFM) expertise to develop a unique solution for managing human and AI agents. Meanwhile, SoundHound can extend conventional conversational AI experiences into smart devices.

However, there is a tension here. Buying capability is easy. Integrating it into a coherent platform is hard. As such, it may take time for these visions to come to life.